1-800-548-4639

1-800-548-4639

If you owe taxes, the Internal Revenue Service (IRS), state or local tax bureau wants to get paid. Sometimes, in an effort to get the money they feel they are owed, revenue departments will make a legal claim, known as a tax lien, against a piece of property you own. Tax liens are meant to guarantee that the tax will get repaid. If you receive notice that the government has placed a lien on your property, there are things you can do to stop the lien and to protect your assets. Learn more about tax liens, what triggers them and what you can do to prevent them.

What Are Tax Liens?

When an individual or company falls behind on taxes, the government can make a claim against property owned by the individual or business. The government’s claim is a tax lien. It is meant to ensure that the government or creditor gets the money it is owed.

A tax lien does not mean that the government is seizing your property or that it will necessarily demand that you sell the property to pay off your tax debt. Instead, it simply means that should you sell the property in the future, the government is entitled to receive a portion of the proceeds, based on the amount of the lien. The tax lien takes precedent over other liens, such a bank, which might also have a claim on the debt.

In some cases, a tax lien precedes a tax levy. While a lien is simply a legal claim, a levy allows the government to seize your property to collect the money it is owed. The government can collect the money it’s owed through a levy by garnishing your wages, freezing your bank account or seizing other assets, such as your car or home.

What Is the Tax Lien Process?

It is unlikely that a tax lien will come out of the blue, without any warning. The government should notify you that you owe taxes and that it wants to be paid. Typically, the warning comes in the form of a letter and a bill known as a Notice and Demand for Payment.

The government sends out the notice after determining that a taxpayer has not paid enough taxes. It might do that after reviewing an individual’s or company’s tax return. If the government thinks that it is owed money, it will charge the amount of taxes due as well as a penalty and interest. Penalties and interest start to accrue on the tax balance from the date it was due and not paid.

After receiving the notice and demand for payment, the taxpayer has a few options. They can pay the amount owed, at which point the case will be closed and no tax lien created. Another option is not to pay the amount demanded. A taxpayer might refuse to pay or may ignore the notice. If that occurs, the government will file a notice to let creditors know that it has a legal claim to a taxpayer’s property.

The lien is then attached to any property the taxpayer owns.

What Is the Impact of a Tax Lien?

Since a tax lien isn’t a demand for payment and isn’t the government collecting on the debt owed, it might not seem like that much of a big deal. In fact, a tax lien can complicate your financial situation, as it is the government’s way of jumping the queue to ensure that it will be paid first. Although tax liens no longer show up on credit reports, they can limit your ability to get a new loan, as the lien would be applied to the collateral on the new loan in addition to any existing property you own.

A tax lien can also complicate the process of selling your home, as it will show up during the title search. Depending on how much equity you have in the house, a lien can keep the sale from going through, as the lender might not get paid after the government takes its share. If you have a considerable amount of equity in the house or own it outright, you’ll get less from the sale of your home if there is a lien on it.

If enough time passes and you still do not pay the tax balance, the government can issue a levy. When that happens, it can take your property and sell it or collect a portion of your wages until the balance is paid in full.

Types of Tax Liens

A lien can be voluntary or involuntary. When a voluntary lien is placed on your property, you are aware of it and give permission for it. When you take out a mortgage to buy a house, the lender places a voluntary lien on the home. If you fall behind on payments, the lender can repossess the property. The same is true of using an auto loan to buy a new car.

A creditor doesn’t need to get your permission before placing an involuntary lien on your property. Tax liens are almost always involuntary. The government isn’t going to call you in advance to see if you approve of it putting a lien on your house or other assets. Instead, it will simply make its claim by applying the lien.

The source of a tax lien depends on the source of the tax issue. If you live in a state with income tax and owe back taxes, your state can apply a lien to your property. If you owe money to the IRS, the federal government can put a lien on your property.

What Are Federal Tax Liens?

Federal tax liens are the U.S. government’s claims against your property when you owe taxes and either refuse or are unable to pay. If the federal government has placed a lien on your property, you have several options for removing it. Otherwise, the lien will remain and the government will be first to collect if you ever sell the asset.

One thing to note is that although filing for bankruptcy often wipes out many of a company’s or individual’s debts, doing so will not remove tax liens.

What Is a State Tax Lien?

A state tax lien is issued by the state where a person lives or does business. Like a federal lien, a state tax lien is a claim on property and assets made when an individual or business has unpaid back taxes. If the tax balance remains unpaid, the state has the right to pursue ways of collecting the money due, including tax liens. Those methods can include garnishing an individual’s wages and freezing bank accounts.

Are There Other Types of Tax Liens?

Several other types of tax liens exist. For example, if an individual or business owns a house or another type of real estate and falls behind on their property tax payments, the municipal or county government can put a property tax lien on the piece of real estate. If the taxes are still not paid, the government can often sell the real estate to pay the property tax bill.

How to Stop Tax Liens

If you have a tax lien on your property, you have several options when it comes to removing it. The quickest way to stop a tax lien is to pay the balance owed. After the balance is paid in full, the IRS will release the lien within 30 days. That can seem easier said than done, especially if you have a hefty tax bill. The IRS does have payment plans available that allow you to repay the debt in small amounts over time. In some circumstances, the government might also be willing to accept what’s known as an offer in compromise.

An offer in compromise allows you to settle your tax debt by paying less than you owe. Often, the amount paid is considerably less than the amount owed. Offers in compromise can be difficult to get, as the IRS is usually convinced that taxpayers are capable of paying the balance in full. If you’re interested in getting rid of an IRS tax lien by arranging for an offer in compromise, it can be helpful to work with experienced tax professionals. BC Tax has worked with countless clients in Colorado and across the U.S., helping them remove tax liens and settle debts by arranging for an offer in compromise.

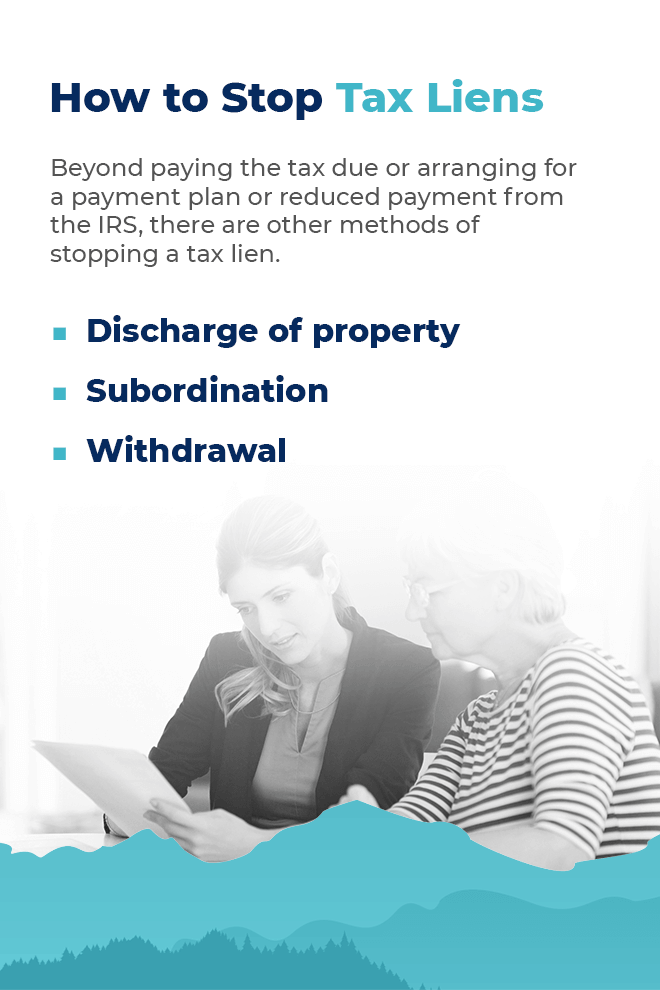

Beyond paying the tax due or arranging for a payment plan or reduced payment from the IRS, there are other methods of stopping a tax lien.

- Discharge of property: Discharge of property takes a tax lien off of a particular asset. For example, if you own a primary residence and a vacation home and are hoping to sell the vacation home, you can petition to have the tax lien taken off of the vacation home. The IRS has specific requirements under which it will allow for a discharge of property. If you own two houses, the IRS may allow for a discharge of property if the value of the house that will keep the lien is at least twice the amount of the balanced owed plus the amount of other debts you have, for example.

- Subordination: Subordination doesn’t stop a lien. What it does is allow for another creditor to jump ahead of the government in line. For example, if you have a mortgage, the mortgage lender is first in line to get paid should you end up selling the property. Once the government issues a tax lien, it jumps ahead of the lender. Now, if you sell the house, the government gets paid first, then the lender gets what is left. If the government agrees to subordination, it would allow the lender to move to the first position. The proceeds of the sale of the house will go first towards the lender, then the government, and any remaining amount goes to you.

- Withdrawal: Withdrawal will take a lien off of an asset or property, ensuring creditors that the government is no longer making a claim to it. Getting a lien withdrawn doesn’t mean you aren’t responsible for paying the debt. The responsibility remains, but typically, the IRS has gotten proof that you will pay the debt. One example of a circumstance in which the IRS might agree to a withdrawal of a lien is if you set up a direct debit payment plan, owe less than $25,000, will repay the full amount within 60 months and make at least three consecutive payments.

How to Prevent Tax Liens

The best way to prevent a tax lien is to file your taxes on time and always pay the full amount you owe. It helps to be proactive about your taxes to avoid a lien. Tax planning and preparation can help you avoid surprise tax bills that are more than you afford to pay, for example. Working with a tax services company can help to ensure that you are claiming the deductions you’re eligible to claim and that you aren’t cutting any corners on your tax return. The more accurate your tax returns are, the more likely you are to pay the amount you owe at tax time, reducing the chance that the IRS or state government will come after you for back taxes owed.

If you do fall behind on your taxes, there are still ways for you to avoid a lien, or at least keep the lien from moving forward. Responding quickly to the Notice and Demand for Payment by paying in full will prevent the lien from going forward. Depending on how much you owe, the IRS might not move forward with the lien if you sign up for an installment repayment plan. Filing an offer in compromise might also help you avoid a tax lien and reduce the amount of tax you need to pay.

Work With BC Tax to Stop Tax Liens

If you’ve received a Notice and Demand for Payment from the IRS or if you’re facing a state tax lien, you do not have to navigate the process on your own. BC Tax works to help people in Colorado and across the United States resolve their tax problems. Whether you’re trying to avoid a lien or remove an existing one, one of our Enrolled Agents will evaluate your situation and recommend the most appropriate way to move forward.

Once your existing tax problems are resolved, we can continue to work with you, offering tax planning and preparation services, to help minimize the chance of future issues coming up. Contact us today to learn more about our process for responding to tax liens and to discover which option will best help you.

Authored by the BC Tax Insights Team, this article reflects the collective expertise and experience of our seasoned tax professionals. The Insights Team at BC Tax comprises specialists with a deep understanding of various tax scenarios and solutions. With a focus on providing informative, accurate, and practical insights, our goal is to guide readers through the complexities of taxation and financial planning. Every piece is crafted with the intent to help individuals and businesses navigate the ever-evolving world of taxes, ensuring clarity and confidence in decision-making.