1-800-548-4639

1-800-548-4639

You work hard to earn your money. You should get to keep as much of it in your wallet or bank account as possible. Although paying the tax you owe is important, so is making sure you don’t pay more tax than necessary. Tax planning helps you reduce your tax bill or defer certain taxes — it can involve saving money in certain accounts to reduce your taxable income or keeping accurate records of any expenses you could deduct from your income.

Tax planning doesn’t just help to lower your tax bill for the year. It can also help you make important financial decisions. For example, tax planning strategies can help you determine if it’s a good time to sell a house or if you should wait. As you get ready for 2020, get ready to make a plan for your tax return.

The Importance of Tax Planning

The tax system in the U.S. is a progressive one — this means, the higher your income, the higher the rate at which your income is taxed. There are seven tax brackets in the U.S., with tax rates ranging from 10 percent to 37 percent.

For example, if you are a single person who has a taxable income of $9,875 or less, your tax rate is 10 percent for the 2020 tax year. If you’re single and earn more than $518,401 in 2020, you would have a tax rate of 37 percent. However, if you’re married and file a joint return with your spouse, the income amount is doubled for each tax bracket.

The 2020 tax brackets for single filers are:

- 10 percent: Tax on income under $9,875.

- 12 percent: Tax on income over $9,875.

- 22 percent: Tax on income over $40,125.

- 24 percent: Tax on income over $85,525.

- 32 percent: Tax on income over $163,300.

- 35 percent: Tax on income over $207,350.

- 37 percent: Tax on income over $518,401.

Since the U.S. tax system is progressive, taxpayers only have to pay the designated tax rate for each bracket. For example, if you have income over $518,401, you don’t have to pay a 37 percent tax on the entire amount of your earned money.

If your income is $600,000 in 2020, you will pay 10 percent on the first $9,875, 12 percent on the amount between $9,875 and $40,124, 22 percent on the amount between $40,125 and $85,524 and so on.

Since the tax rate increases with each tax bracket, ending up in a lower bracket means getting to pay a lower rate. With the right tax planning methods and strategies in place, you can reduce your taxable income, so you fall into a lower bracket.

Tax planning does more than help you pay fewer taxes by reducing the amount of taxable income. It can also help to ensure you pay the right amount of taxes. If you don’t pay enough in tax to the Internal Revenue Service (IRS) for the year, you can find yourself facing an underpayment penalty. You might pay too little in taxes if your employer doesn’t withhold enough from your paychecks or if you make estimated payments and don’t pay enough over the course of the year.

To avoid the underpayment penalty, you need to pay either 100 percent of your tax liability for the previous year or 90 percent of your tax liability for the current year, whichever amount is lower. Knowing how much you owed last year or how much you expect to earn in 2020 will help you make sure to pay enough to the IRS and avoid the penalty.

Tax planning can also be a part of your overall financial plan. If you find legitimate ways to reduce your taxable income, you have more money to put toward things that matter to you, such as saving for a new home or contributing to your retirement.

You can also use tax planning to guide you as you make financial decisions. For example, if you’re planning on getting married in 2020, understanding how your marriage will change your financial and tax situation can help you determine when to make certain decisions, such as buying or selling a home.

Tax Planning Throughout 2020

Although many people think tax planning is a project best left for the first and last quarters of the year, there are steps you can take throughout the entire year to help keep your tax bill as low as possible:

Before April 15: Prepare and Review Your 2019 Tax Return

At the beginning of 2020, you’ll begin to receive paperwork from a variety of sources to use as you prepare your 2019 tax return. If you are employed by a company, it should send you a Form W-2 by the end of January. If you work as an independent contractor, your clients should send you a 1099-MISC by the end of January as well. You might also get 1099 forms from your bank if you earned interest, plus forms from any investment companies you work with, your mortgage company and the institutions that manage your student loans.

Although the “year” officially ends on December 31, 2019, it’s still possible to do some last-minute, year-end tax planning for 2019 during 2020. Several tax-advantaged savings accounts have a contribution deadline of April 15, 2020, rather than December 31, 2019. A tax-advantaged account is one that lets you deduct the amount you contribute from your taxable income for the year. You have until April 15 to make 2019 contributions to:

- An individual retirement account (traditional or Roth IRA).

- A health savings account (HSA).

- An educational savings account or 529 plan.

For 2019 and 2020, you can contribute up to $6,000 to an IRA for the year. If you make contributions to a traditional IRA before April 15, you can deduct the amount from your 2019 income. If you’ve already contributed the full $6,000 for 2019, you can begin saving for 2020 before April 15. However, you’ll need to tell the institution you want your pre-April 15 contributions to count towards 2020, not 2019.

In the case of an HSA, you can contribute up to $3,500 for 2019 if you have an individual health insurance plan or up to $7,000 if you have a family plan with the appropriate deductible. If you’d like to lower your taxable income by contributing to an educational savings account, you can contribute up to $2,000 per beneficiary. There’s no limit on the number of beneficiaries.

After reducing your taxable income for 2019 and filing your return, you can use the information on it to help plan your 2020 tax strategy.

Tax Planning From January Through December

If you got a refund on your 2019 return, it might be a good idea to adjust the amount your employer withholds from your paycheck each period. Although getting that windfall of cash around April 15 is nice, you might find that getting a bigger paycheck helps you budget and plan for purchases better.

You can adjust the amount that’s taken out from your paychecks by asking your employer for a new Form W-4. The IRS is updating Form W-4 for 2020. With the new form, you can estimate your deductions for the year to decrease the amount that’s withheld from your pay.

It’s also a good idea to read over Form 1040 to see what deductions are available to you in 2020. For example, you might be able to subtract student loan interest if you recently graduated and now have student loans. If you recently adopted or gave birth to a child, you might be able to claim a deduction for them.

Keep organized records throughout the year, so you have documentation of any deductions you hope to claim on your 2020 return. Create a file for receipts.

End-of-Year Tax Planning

Starting in October, it’s time to shift your tax planning into high gear. Now’s the time to assess your situation and to figure out what you can do to reduce your tax liability for the year. You might decide to increase your charitable contributions, which can increase the amount of itemized deductions you’re eligible to deduct.

If you have investments that aren’t doing well, you might want to sell them before the year is up, so you can claim the loss on your 2020 return. The end of the year can also be the time to maximize your contributions to a 401(k) or another employer-sponsored retirement plan.

Tax Planning Tips for 2020

As you get ready to plan for next year’s tax return today, keeping the following in mind will help to lower your tax bill:

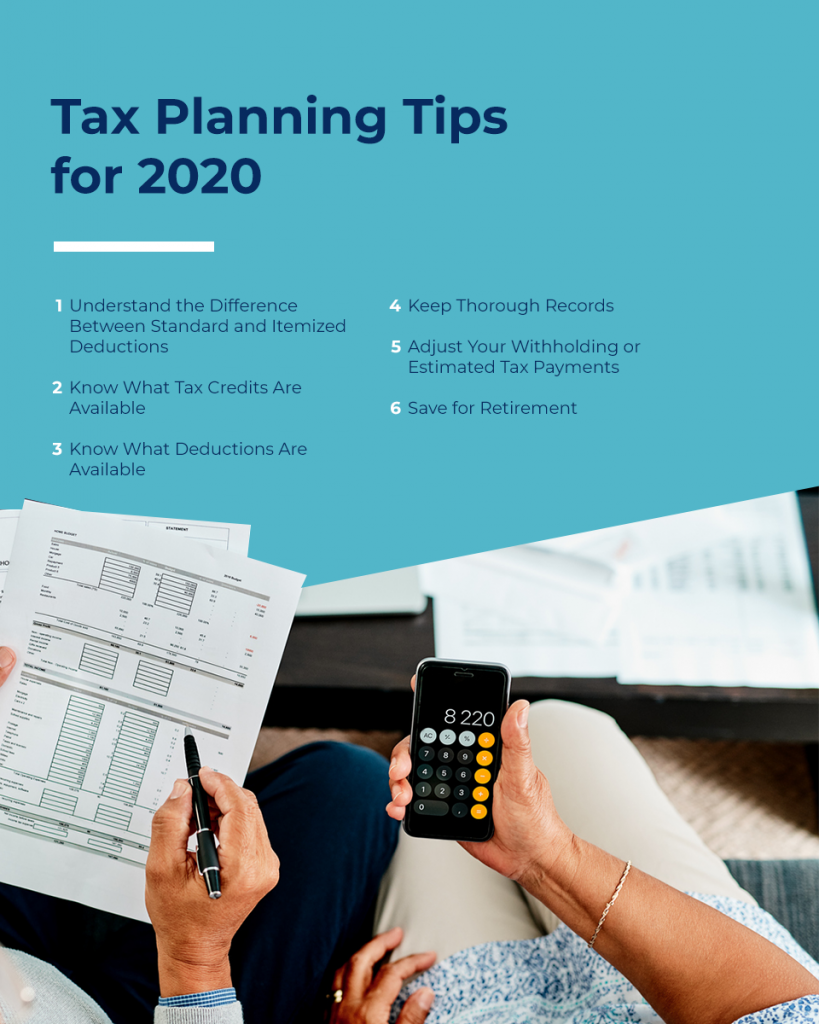

1. Understand the Difference Between Standard and Itemized Deductions

When you file your tax return, you have the option of claiming either the standard deduction or itemizing your deductions. For 2020, the standard deduction is $12,400 for single taxpayers or for married couples who file separately. Married couples who file jointly can claim a deduction of $24,800 in 2020.

Although the standard deduction is the right choice for many taxpayers, there is a chance that you could lower your tax bill by itemizing your deductions instead. To itemize deductions, you need to complete an additional form — Schedule A — when completing your tax return. You also need to have records for each of the deductions you claim. Itemizing deductions makes sense if the amount of your deductions ends up being more than the standard deduction.

Potential itemized deductions for 2020 include:

- Mortgage interest payments.

- State or local income or sales tax.

- Property taxes.

- Medical expenses that are more than 10 percent of your income.

- Contributions and donations to charity.

2. Know What Tax Credits Are Available

Tax credits reduce the amount of tax you need to pay (compared to deductions, which reduce the amount of your taxable income). Understanding your options when it comes to tax credits can help you make the best plan for your taxes. Some examples of tax credits are:

- American Opportunity Credit for education-related expenses.

- Lifetime Learning Credit for college costs.

- Adoption credit.

- Child credit.

- Child and dependent care credit.

- Saver’s Credit for contributing to retirement if your income is below a certain amount.

- Earned Income Credit.

- Residential Energy Tax Credit.

If you have children, paid for education or installed a solar energy system — or plan to do so — in 2020, you might be eligible for one or more credits on your tax return. Being aware of each credit can also help you determine whether 2020 is the year you make a life change, such are returning to college, adopting a child or starting to save for retirement.

3. Know What Deductions Are Available

Whether you itemize deductions or take the standard deduction on your return, there are a few additional deductions you might claim to reduce your taxable income. Unlike itemized deductions, you don’t need to fill out Schedule A to claim the following:

- Student loan interest deduction.

- IRA deduction.

- Educator expenses deduction.

- Health insurance deduction if self-employed.

- HSA deduction.

- Moving expenses if you’re in the Armed Forces.

Certain deductions have income limits, so you might not be able to claim them if you make above a certain amount.

4. Keep Thorough Records

While you don’t have to submit receipts of expenses with your tax return, it’s still a good idea to keep records and to hang on to any receipts or other proof that you have certain deductions throughout the year. To make things easier on yourself at tax-time, file receipts as you get them and make a note of any expenses you might deduct as the year goes on.

If the IRS audits you, you will most likely need to provide it with proof and documentation to verify your deductions and the amount of your taxable income.

5. Adjust Your Withholding or Estimated Tax Payments

Don’t be shy about adjusting your paycheck withholding if you regularly get a tax refund. If you’re self-employed and make estimated tax payments, make those payments based on what you earned during each quarter, rather than blindly guessing and hoping for the best.

It’s a smart idea to take a look at your paystub each period to make sure your employer is withholding the appropriate amount from your check. The IRS has a withholding calculator you can use to see if the right amount is being subtracted from your pay. Some people might benefit from adjusting their withholding, such as:

- Married couples, especially if both partners work.

- People who work multiple jobs.

- People with self-employed income.

- People who work on a very part-time or seasonal basis.

- People with high incomes.

- People with lots of deductions, schedules or otherwise complicated tax returns.

6. Save for Retirement

Saving for retirement helps with your tax planning in several ways. Contributing to a traditional IRA, 401(k) or another employer-sponsored plan can reduce the amount of your taxable income for the year. If you decide to contribute to a Roth IRA, you need to pay tax on the contributed amount, but you won’t have to pay tax when it is time to withdraw the money during your retirement. You also don’t pay tax on the earnings in a Roth IRA.

If you can, contribute up to the limit to a 401(k), IRA or both. If you can’t save that much, set aside as much as you can. If your employer matches your 401(k) contributions, try to save enough to get the full amount of the match. You won’t have to pay tax on the money until you retire.

Contact BC Tax for 2020 Tax Planning

For nearly 20 years, BC Tax has been one of the top tax resolution firms in the U.S. Although we’re based in Colorado, we help clients from all over the country and around the world overcome challenging tax situations. Our countless success stories speak for themselves.

In addition to helping our clients resolve tax concerns, we also provide tax planning and preparation services. We can help you create a tax planning strategy that reduces your tax bill and helps you keep more of your hard-earned money. To learn more about what we do, contact us today.

Our Tax Planning Services:

Authored by the BC Tax Insights Team, this article reflects the collective expertise and experience of our seasoned tax professionals. The Insights Team at BC Tax comprises specialists with a deep understanding of various tax scenarios and solutions. With a focus on providing informative, accurate, and practical insights, our goal is to guide readers through the complexities of taxation and financial planning. Every piece is crafted with the intent to help individuals and businesses navigate the ever-evolving world of taxes, ensuring clarity and confidence in decision-making.