1-800-548-4639

1-800-548-4639Tax Forgiveness Fresh Start Program

The Internal Revenue Service (IRS) has several initiatives to help taxpayers who owe back taxes. The programs can give you a “fresh start” by reducing your tax bill or making it easier to pay what you owe. Tax relief programs from the IRS are a win-win situation. If you qualify to participate in the Fresh Start initiative, you can avoid hefty tax penalties, liens or jail time. The IRS benefits because it can collect some of what’s owed.

If you owe the IRS and are looking for help, check out the Fresh Start program, and see if you qualify.

What Is the Fresh Start Initiative?

The IRS created the Fresh Start program in 2011 to help businesses and individuals facing difficulty paying their taxes. The program’s goal is to help taxpayers get in good standing with the IRS. Its focus is rehabilitation rather than punishment or penalty.

Depending on the Fresh Start route you take, the program might reduce the amount you owe the IRS, freeze the debt or help you avoid a tax lien. A key feature of Fresh Start is it prevents the IRS from collecting more from you than you can afford to pay.

By creating Fresh Start, the IRS made it easier for taxpayers to qualify for relief programs. If you owe back taxes, BC Tax can work with you to help you choose the IRS Fresh Start program that best meets your needs and will provide you with the greatest amount of tax relief.

IRS Fresh Start Program Requirements

The requirements to participate in the Fresh Start initiative vary based on the specific program you want to enroll in. Requirements also vary depending on if you’re an individual or business owner.

The IRS has income limits and maximum tax owed limits for the Fresh Start program. If you are a single tax-filer, your income typically needs to be less than $100,000 to qualify. If you are a self-employed business owner, you need to demonstrate a significant reduction in business income before participating in the program.

You also need to be up to date on filing your tax returns to qualify for Fresh Start.

Generally speaking, the Fresh Start program might be right for you if you owe back taxes and are having trouble paying them. If it’s unlikely you’ll be able to pay your taxes, the IRS might allow you to apply for Currently Non-Collectible (CNC) status or for an Offer in Compromise. If you can pay your taxes but need more time, a payment plan or installment agreement might be right for you.

IRS Forgiveness Program Options

Four programs fall under the general Fresh Start umbrella. The IRS won’t guide you toward the program that’s most appropriate for you. It’s up to you to determine which option will provide you with the most relief or which one you’re eligible for. Working with a tax professional, such as the team of enrolled agents at BC Tax, can make you more likely to choose the Fresh Start program that will provide you with the greatest amount of relief.

1. IRS Offer in Compromise

The Fresh Start program expanded the eligibility for the IRS’ Offer in Compromise program(OIC). Under an OIC, the taxpayer and IRS agree on a settlement amount typically less than what the taxpayer owes. To qualify for the program, you need to demonstrate to the IRS that you can’t afford to pay the total amount of back taxes.

To generally qualify for an OIC, you need to do the following:

- File all required tax returns.

- Have a bill for a tax debt.

- Make all required estimated tax payments (if applicable).

- Make all required tax deposits for the current quarter and previous two quarters if you operate a business with employees.

You can’t be in a bankruptcy proceeding when you apply for an OIC. You also can’t be able to pay your tax debt in full when you apply.

The Fresh Start program expanded eligibility for an OIC. Under the program, the IRS relaxed requirements for:

- Student loan payments: Under the Fresh Start program, you can continue to make payments on student loans when you have an OIC.

- Delinquent state taxes: The Fresh Start program also allows you to pay delinquent state and other taxes when you participate in an OIC.

- Allowable living expenses: The IRS increased the number of allowable expenses and added more categories for living expenses.

- Reasonable collection potential: The IRS looks at one year of future income when determining the reasonable collection potential for OICs paid within five months. It was previously four years. It also uses two years of potential income for OICs paid in six to 25 months instead of five years.

If you qualify for an OIC and the IRS accepts your application, you have two repayment options. You can make a lump-sum payment or periodic payments.

With the lump sum option, you make a 20% payment when you submit the application. If the IRS accepts your OIC, you’ll get written confirmation. You then have to pay the remaining balance in five payments or fewer.

If you decide to make periodic payments, you send in an initial payment with the OIC application. You then continue to pay in monthly installments while the IRS reviews your application. If your OIC is accepted, you keep making monthly payments until you’ve paid off the agreed-upon amount.

The IRS could reject your OIC application. Working with a tax professional before starting the application process reduces the likelihood of rejection and helps you get out of a tax debt faster.

2. Installment Agreement

The installment agreement option existed before the Fresh Start initiative began, but the program underwent several changes. Under the Fresh Start program, individual taxpayers can qualify for a 72-month (six-year) installment agreement when they owe less than $50,000. Business taxpayers can qualify if they owe less than $25,000.

When you apply for an installment agreement, the IRS can’t issue a levy against you and can’t attempt to collect from you while your application is being processed. If your application is accepted, you need to pay the agreed-upon amount every month until you’ve paid the balance in full, within 72 months.

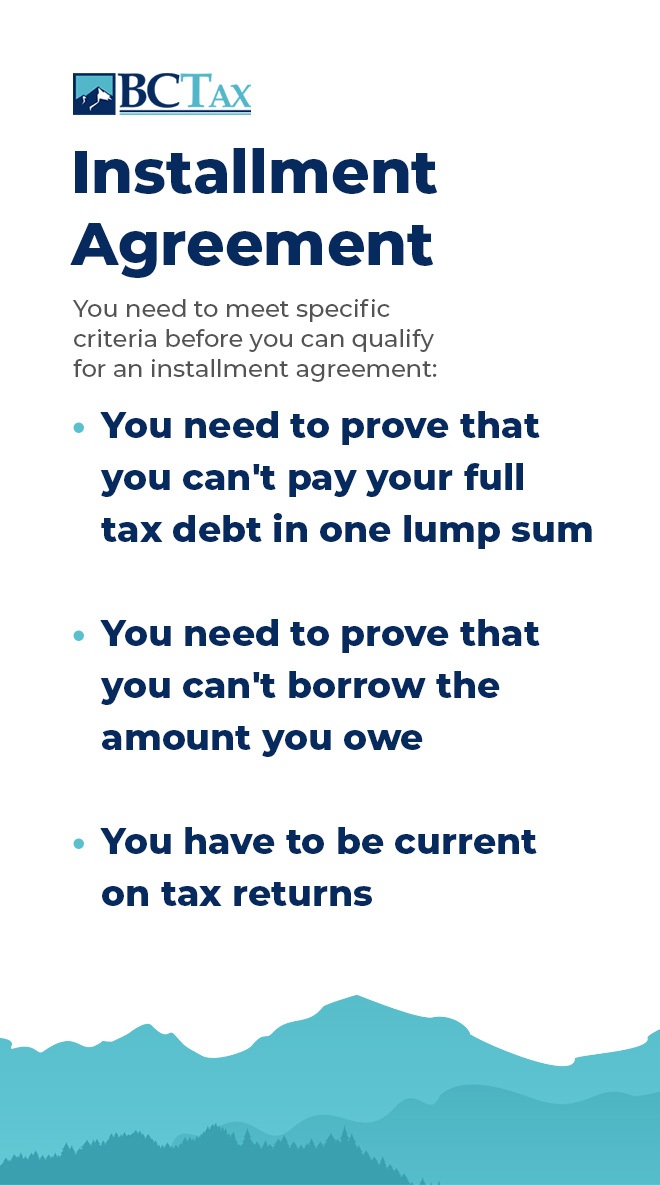

You need to meet specific criteria before you can qualify for an installment agreement:

- You need to prove that you can’t pay your full tax debt in one lump sum: You need to tell the IRS about all the cash and assets you have — including retirement accounts — to demonstrate you don’t have the cash to pay off your tax debt.

- You need to prove that you can’t borrow the amount you owe: You have to demonstrate that you can’t borrow the money you owe the IRS, such as taking out a personal loan or home equity loan.

- You have to be current on tax returns: All of your tax returns must be filed and up-to-date.

How much the installment agreement costs you depends on the type of plan you choose and how you pay for it. If you’re an individual whose balance is more than $25,000 and you need a long-term installment agreement, you’ll pay a set-up fee of $31 for a direct debit plan. Every month, the payment gets pulled from your checking account automatically. You’ll also have to pay any interest or accrued penalties on the tax debt.

If you owe less than $25,000 and don’t want to sign up for automatic monthly payments, you can pay a set-up fee of $130 for a non-direct debit payment plan. Under the plan, you schedule payments yourself, either directly from your bank account or by card. You also have to pay interest and penalties, in addition to the tax debt.

Business taxpayers pay the same set-up fees and any accrued interest or penalties. The tax debt limit for businesses is lower than for individuals, though. If your business owes more than $10,000, you need to sign up for the automatic direct debit payment option.

Work with a tax professional when applying for an installment agreement to ensure you choose the right plan for you.

Installment Agreement Assistance

3. Penalty and Tax Lien Relief

When taxpayers fall behind on taxes, the IRS typically tacks interest onto the unpaid tax. It also charges taxpayers penalties for late payments or failure to file. The failure-to-pay penalty is 0.5% per month, up to 25% of the tax owed. The penalty keeps accruing until the debt is paid.

It’s possible to get relief from tax penalties through a process called penalty abatement. When the Fresh Start program first launched, the IRS offered penalty abatement to self-employed taxpayers and had a 25% decrease in income or to wage earners who were unemployed for at least 30 days.

Penalty relief is still available, but you need to demonstrate reasonable cause to qualify. The IRS considers any reasons that demonstrate that you made every effort to pay your taxes but weren’t able to.

Some examples of reasonable cause for penalty abatement include:

- Serious illness, unavoidable absence or death of the taxpayer or an immediate family member

- Natural disaster, fire or another disruption

- Inability to get access to your records

When applying for penalty relief due to reasonable cause, you need to provide evidence. Documentation of a natural disaster or fire might be required, or a letter from a hospital or physician that proves that you or an immediate family member were incapacitated or severely ill. The letter should include the start and end date of the incapacitation or illness.

An enrolled agent at BC Tax can help you win penalty relief when needed.

Similarly, the Fresh Start program offers tax lien relief. Thanks to Fresh Start, you need to owe $10,000 or more before the IRS can file a Notice of Federal Tax Lien. If you set up an installment agreement, the IRS should withdraw its notice as long as you request the withdrawal. The IRS also needs to withdraw the notice once you’ve paid the debt in full.

4. Currently Non-Collectible Status

The Fresh Start program eased the application process for currently non-collectible (CNC) status, particularly for taxpayers who owe less than $10,000.

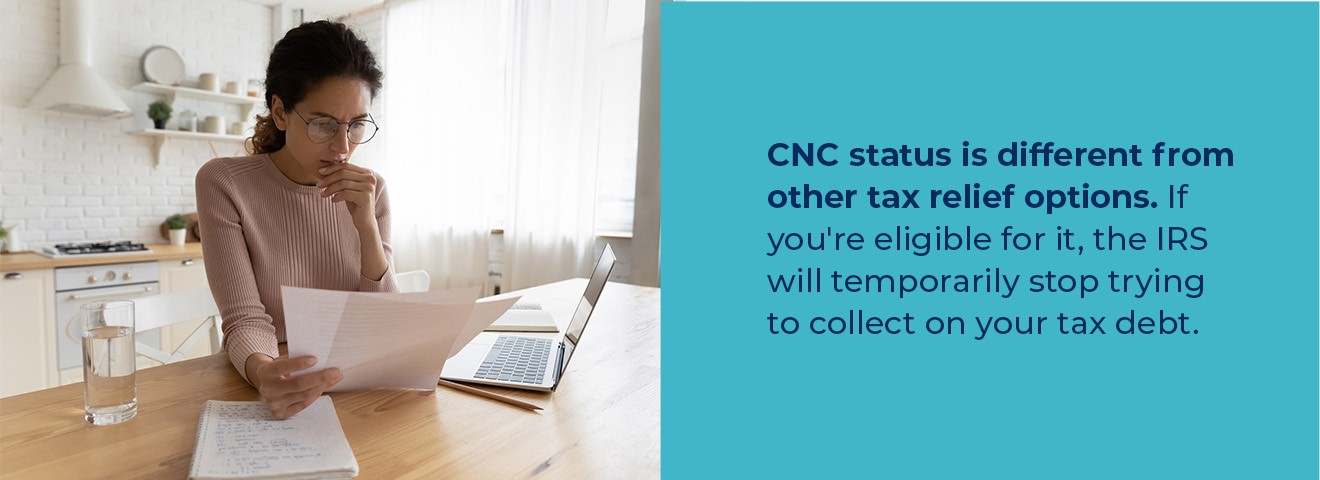

CNC status is different from other tax relief options. If you’re eligible for it, the IRS will temporarily stop trying to collect on your tax debt. You aren’t free from having to pay the debt ever, you’re just free from having to worry about it at the moment.

You need to provide the IRS with documentation of your assets and income when you apply for CNC status. Essentially, your documents should show that you have no reasonable way to pay your tax debt in the moment. If you don’t have savings and have a low income at the moment, you’re likely to qualify for CNC status. Generally, the IRS won’t try to collect from you if you don’t have enough income or savings to cover the cost of reasonable living expenses.

Once you get CNC status, the IRS will typically review your financial situation each year to verify you remain eligible. If you have a change in finances, such as earning more money or inheriting money, you might lose CNC status and have to repay taxes. Alternatively, you might remain in CNC status long enough that the statute of limitations on your tax debt expires, and you are no longer responsible for the debt.

Before you qualify for CNC status, you need to be up-to-date on your tax returns. You’ll also have to continue to file tax returns while you are in CNC status. If you get a tax refund, the IRS can keep it and apply it to your existing tax debt.

The enrolled agents at BC Tax can help you get current on your tax returns and can evaluate your income and assets to see if CNC status, or another option, such as an installment agreement, would be right for you. We’ll communicate with the IRS on your behalf throughout the process.

How to Apply for the IRS Fresh Start Program

If you need a fresh start or one-time forgiveness from the IRS, the first step is to decide which tax relief option is best for you, whether it’s CNC status, an installment agreement or an offer in compromise. Working with a tax professional allows you to choose the most appropriate option, reducing the chance of rejection.

The application process varies based on the program you end up choosing. At BC Tax, we’ll work with you to help you gather the necessary paperwork to submit a strong application.

Contact BC Tax to Get a Fresh Start

BC Tax can help you get a fresh start on your taxes, whether you’re an individual or a business taxpayer. We work with you and the IRS to determine which tax relief solution is best for your situation. We communicate with the IRS on your behalf, helping to reduce your stress and ensuring a smoother application process.

Contact us today to learn more about our tax services and how our enrolled agents can help you negotiate with the IRS to reduce or avoid penalties, wage garnishment or legal actions.

Authored by the BC Tax Insights Team, this article reflects the collective expertise and experience of our seasoned tax professionals. The Insights Team at BC Tax comprises specialists with a deep understanding of various tax scenarios and solutions. With a focus on providing informative, accurate, and practical insights, our goal is to guide readers through the complexities of taxation and financial planning. Every piece is crafted with the intent to help individuals and businesses navigate the ever-evolving world of taxes, ensuring clarity and confidence in decision-making.