1-800-548-4639

1-800-548-4639If you’re a freelancer, self-employed or own a business, you may be responsible for making estimated tax payments to the Internal Revenue Service (IRS) throughout the year. These payments are used to cover your federal income tax liability and are typically made quarterly. However, many people are unfamiliar with the concept of estimated tax payments and how they work.

Below, we’ll explain what estimated tax payments are, who needs to make them, how to calculate them and when to submit them to the IRS. We’ll also cover some tips and best practices for managing your estimated tax payments to avoid penalties and interest.

What Is an IRS Estimated Tax Payment?

An IRS estimated tax payment is a payment made to the IRS by individuals or businesses that do not have taxes withheld from their income or have not had enough taxes withheld to cover their tax liability.

The purpose of estimated tax payments is to ensure taxpayers meet their tax obligations throughout the year rather than waiting until tax season to pay their taxes in full. Estimated tax payments are typically made quarterly, with due dates in April, June, September and January of the following year. The amount of the estimated tax payment is calculated based on your expected income and tax liability for the year.

If you fail to make the required estimated tax payments, you may be subject to penalties and interest on the underpayment. However, there are certain exceptions and safe harbor provisions that can apply, such as if you had no tax liability in the previous year or if you paid at least 90% of your current year’s tax liability through estimated tax payments. As a result, it’s important to understand your estimated tax payment obligations and make payments on time to avoid penalties and interest.

How Does Estimated Tax Payment Work?

To make estimated tax payments, you must approximate your expected income and tax liability for the year and then make payments based on these estimates. You can use Form 1040-ES, Estimated Tax for Individuals, to calculate and make your estimated tax payments. This form includes worksheets to help you estimate your income, deductions and tax liability for the year.

Estimated tax payments are typically made quarterly. If you underestimate your tax liability and fail to make the required estimated tax payments, you may be subject to penalties and interest on the underpayment, though certain exceptions can apply.

You can make estimated tax payments using several methods, such as:

- Online payments through the Electronic Federal Tax Payment System (EFTPS)

- Paying by phone using the EFTPS Voice Response System

- Mailing a check or money order to the IRS

- Using the IRS’s Direct Pay online system

Estimated tax payments are separate from annual income tax returns, which are typically filed in April of the following year. If you make estimated tax payments, you will still need to file an annual income tax return to reconcile your estimated tax payments with your actual tax liability for the year.

Why Am I Being Asked to Pay Estimated Taxes?

You may be asked to pay estimated taxes if you receive income that is not subject to tax withholding or if you do not have enough taxes withheld from your income to cover your tax liability. Some common reasons why you may be asked to pay estimated taxes include:

- Self-employment income: If you are self-employed, you are generally responsible for paying your own taxes. You’ll estimate your expected income and tax liability for the year and make quarterly estimated tax payments.

- Rental income: If you receive rental income from a property you own but do not have enough taxes withheld from the rental income, you may be required to make estimated tax payments.

- Investment income: If you receive income from investments, such as dividends or capital gains, you may be required to make estimated tax payments if you do not have enough taxes withheld from the investment income.

- Other income: If you receive income from other sources that are not subject to tax withholding, such as alimony, prizes or awards, you may be required to make estimated tax payments.

Who Needs to Pay Estimated Tax?

Individuals, partners, sole proprietors and S corporation shareholders generally should pay estimated taxes if they anticipate to owe $1,000 or more in taxes for the current tax year after subtracting any withholding and refundable credits.

More specifically, if you receive income that is not subject to tax withholding like self-employment income, rental income, investment income or other types of taxable income, you may need to make estimated tax payments. This is because there is no employer or payer withholding taxes from these types of income, and you are responsible for paying the taxes yourself.

Additionally, if you are employed but do not have enough taxes withheld from your paycheck to cover your tax liability, you may need to make estimated tax payments. This can happen if you have a significant amount of income from other sources, such as self-employment income, or if you have significant deductions or credits that reduce your tax liability.

Who Doesn’t Have to Pay Estimated Tax?

Some taxpayers may be exempt from making estimated tax payments, including:

- Employees who have sufficient tax withheld from their wages: If you are an employee and have sufficient taxes withheld from your paycheck to cover your tax liability, you may not be required to make estimated tax payments.

- Retirees who receive social security and pension benefits: If your income consists mainly of social security benefits, pensions and other retirement income and you have sufficient taxes withheld from your payments, you may not be required to make estimated tax payments.

- Individuals who expect to owe less than $1,000 in taxes: If you expect to owe less than $1,000 in taxes for the current tax year, you may not be required to make estimated tax payments.

- Farmers and fishermen: If you earn at least two-thirds of your income from farming or fishing, you may be eligible for a special estimated tax payment rule that allows you to pay all of your estimated taxes in one lump sum in January of the following year. For 2023 estimated taxes, this due date is January 16, 2024.

- Newly retired individuals: If you retired during the current tax year and did not make estimated tax payments during the year, you may be exempt from making estimated tax payments for the current tax year.

Note that even if you are exempt from making estimated tax payments, you’re still required to pay any tax liability you owe by the tax filing deadline to avoid penalties and interest on the underpayment.

How to Calculate Estimated Tax

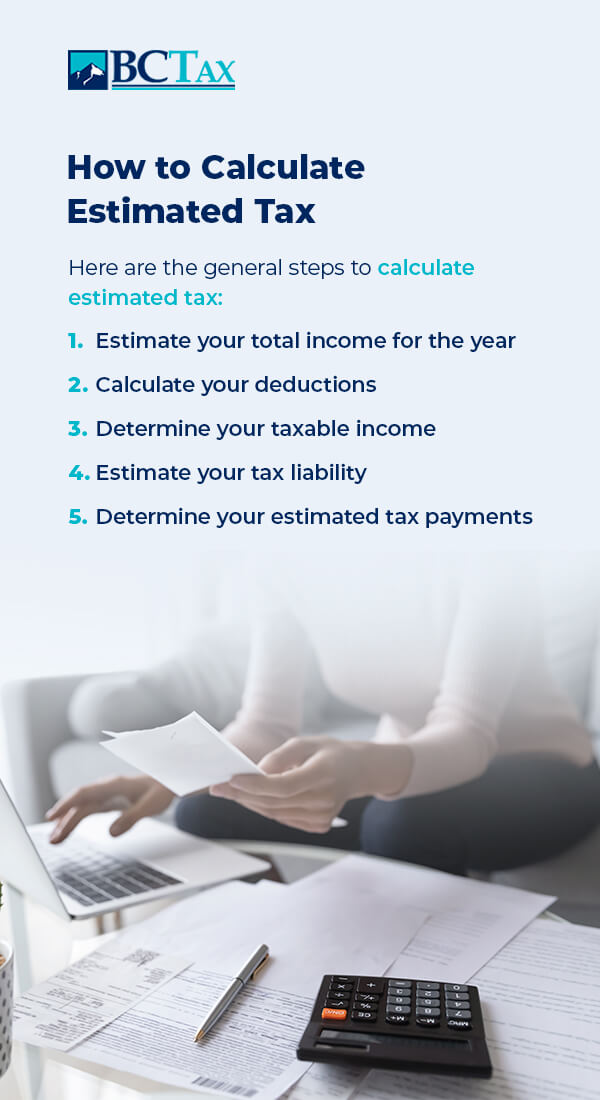

To calculate your estimated tax payments, you will need to estimate your income, deductions and tax liability for the current tax year. Here are the general steps to calculate estimated tax:

- Estimate your total income for the year: This includes all taxable income you expect to receive during the year, such as wages, self-employment income, interest, dividends and rental income.

- Calculate your deductions: This includes any deductions you expect to take, such as the standard deduction, itemized deductions and deductions for self-employment taxes.

- Determine your taxable income: Subtract your deductions from your estimated total income to arrive at your estimated taxable income.

- Estimate your tax liability: Use the tax rates and brackets for the current tax year to estimate your federal income tax liability.

- Determine your estimated tax payments: Subtract any tax credits and other payments you expect to make during the year, such as withholding from wages or estimated tax payments made earlier in the year. The remaining amount is your estimated tax payment for the current quarter.

Note that if you underpay your estimated tax, you may be subject to penalties and interest on the underpayment. Estimate your tax liability accurately and make timely payments to avoid penalties and interest.

When Are Estimated Taxes Due?

Estimated tax payments should be paid four times a year. For most taxpayers, the general due dates are:

- April 15 for the first quarter (covering January 1 through March 31)

- June 15 for the second quarter (covering April 1 through May 31)

- September 15 for the third quarter (covering June 1 through August 31)

- January 15 of the following year for the fourth quarter (covering September 1 through December 31)

These due dates may be different for taxpayers who have a fiscal year rather than a calendar year. Additionally, if the due date falls on a holiday or weekend, the payment is due on the next business day.

If you miss one of the estimated tax payment due dates, you can still make a payment as soon as possible to avoid penalties and interest on the underpayment. You can use Form 1040-ES, Estimated Tax for Individuals, to make estimated tax payments. The form includes a payment voucher you can mail with your payment. Alternatively, you can make payments electronically using the IRS’s EFTPS.

Can Taxpayers Pay Estimated Taxes Anytime?

You can generally pay estimated taxes anytime throughout the year, as long as you make the payments on or before the due dates for each quarterly payment period.

What Is the Penalty for Underpayment of Estimated Tax?

If you fail to make sufficient estimated tax payments throughout the year and owe a significant amount of tax when you file your tax return, you may be subject to an underpayment penalty. The penalty is calculated based on the difference between the amount of tax you should have paid through estimated tax payments and the amount you actually paid.

The penalty is calculated using Form 2210, which is the Underpayment of Estimated Tax by Individuals, Estates, and Trusts form. There are several methods to calculate the penalty, and the IRS will assess the penalty based on the most appropriate method.

The penalty rate is generally the current federal short-term rate plus 3%, and the penalty is assessed on a quarterly basis. The penalty for underpayment of estimated tax can be significant, so it’s crucial to stay on top of your estimated tax payments to avoid owing a large amount at the end of the tax year.

If you’re unsure about how much estimated tax to pay, you may want to use the IRS’s online Estimated Tax Worksheet to help you calculate your payment or consult with a tax professional at BC Tax.

Can I Avoid an Underpayment Penalty?

Yes, there are several ways to avoid an underpayment penalty for not paying enough estimated taxes throughout the year.

One way to avoid the underpayment penalty is to pay at least 90% of your current year’s tax liability through estimated tax payments or through withholding from your wages. If you pay at least 90% of your current year’s tax liability, you generally won’t owe an underpayment penalty, even if you still owe some additional tax when you file your return.

Another way to avoid the underpayment penalty is to pay at least 100% of the prior year’s tax liability through estimated tax payments or through withholding from your wages. This is known as the safe harbor rule and can be used to avoid the underpayment penalty if you’re unable to accurately estimate your current year’s tax liability.

If your income or tax situation changes significantly during the year, you may need to adjust your estimated tax payments to avoid the underpayment penalty. For example, if you receive a large bonus or capital gain later in the year, you may need to make an additional estimated tax payment to avoid the penalty.

Consult with a tax professional from BC Tax to help you calculate your estimated tax payments and avoid any potential underpayment penalties. We may also be able to help you pursue penalty relief.

How BC Tax Can Help With Estimated Taxes

At BC Tax, we can help you with estimated taxes in several ways. Here are some of the services we offer:

- Estimated tax calculations: We can help you calculate your estimated tax payments accurately. We can review your income, deductions and tax liability for the year to help you estimate the right amount of tax to pay each quarter.

- Estimated tax payment reminders: We can remind you when your estimated tax payments are due so you don’t miss any deadlines. We can also help you set up automatic payments to make the process easier.

- Penalty abatement: If you have already missed an estimated tax payment deadline and have been charged penalties and interest, we can help you negotiate with the IRS to reduce or eliminate these penalties.

- Tax planning: We can help you plan ahead to minimize your tax liability for the year. By reviewing your income and deductions, we can help you identify opportunities to reduce your tax bill and make the most of available tax credits and deductions.

- Tax resolution: If you are struggling to pay your estimated tax payments or have other tax issues, we can help you find a resolution. We can work with the IRS on your behalf to negotiate a payment plan or settle your tax debt for less than you owe.

Our services can help you stay on top of your tax obligations and avoid penalties and interest on underpayments. Contact us at BC Tax to learn more about how we can help.

Authored by the BC Tax Insights Team, this article reflects the collective expertise and experience of our seasoned tax professionals. The Insights Team at BC Tax comprises specialists with a deep understanding of various tax scenarios and solutions. With a focus on providing informative, accurate, and practical insights, our goal is to guide readers through the complexities of taxation and financial planning. Every piece is crafted with the intent to help individuals and businesses navigate the ever-evolving world of taxes, ensuring clarity and confidence in decision-making.